Check the preparers qualifications. 2. Use the IRS directory of federal tax return preparers with credentials and select qualifications to find a preparer with the qualifications that you prefer. 3. Ask about service fees. 4. Avoid preparers who base fees on a percentage of the refund or who boasts the bigger refunds than their competitions. 5. Make sure the preparer is available. 6. Prerecords and receipts. 7. Don't use a preparer who will e-file their return using their last pay stub instead of a form w2. 8. Review before signing a tax return. 9. Check with the preparer if something is not clear. 10.

PDF editing your way

Complete or edit your form 14157 anytime and from any device using our web, desktop, and mobile apps. Create custom documents by adding smart fillable fields.

Native cloud integration

Work smarter and export irs form 14157 directly to your preferred cloud. Get everything you need to store, synchronize and share safely with the recipients.

All-in-one PDF converter

Convert and save your irs form 14157 a as PDF (.pdf), presentation (.pptx), image (.jpeg), spreadsheet (.xlsx) or document (.docx). Transform it to the fillable template for one-click reusing.

Faster real-time collaboration

Invite your teammates to work with you in a single secure workspace. Manage complex workflows and remove blockers to collaborate more efficiently.

Well-organized document storage

Generate as many documents and template folders as you need. Add custom tags to your files and records for faster organization and easier access.

Strengthen security and compliance

Add an extra layer of protection to your 14157 form by requiring a signer to enter a password or authenticate their identity via text messages or phone calls.

Company logo & branding

Brand your communication and make your emails recognizable by adding your company’s logo. Generate error-free forms that create a more professional feel for your business.

Multiple export options

Share your files securely by selecting the method of your choice: send by email, SMS, fax, USPS, or create a link to a fillable form. Set up notifications and reminders.

Customizable eSignature workflows

Build and scale eSignature workflows with clicks, not code. Benefit from intuitive experience with role-based signing orders, built-in payments, and detailed audit trail.

Award-winning PDF software

How to prepare Form 14157

1

Open up the Form 14157

Open the form in the editor without downloading/adding the document. All editing instruments can be found online through the gadget.

2

Fill out the file

The editor enables you to change the form's content or just fill out the current fields. You can add an electronic signature and ensure the file is legitimately binding.

3

Save and share the doc

Click DONE to save the edits. You can access the form in your account and share it with others by e mail, fax and Text messages or USPS. Download the document to the computer if necessary.

About Form 14157

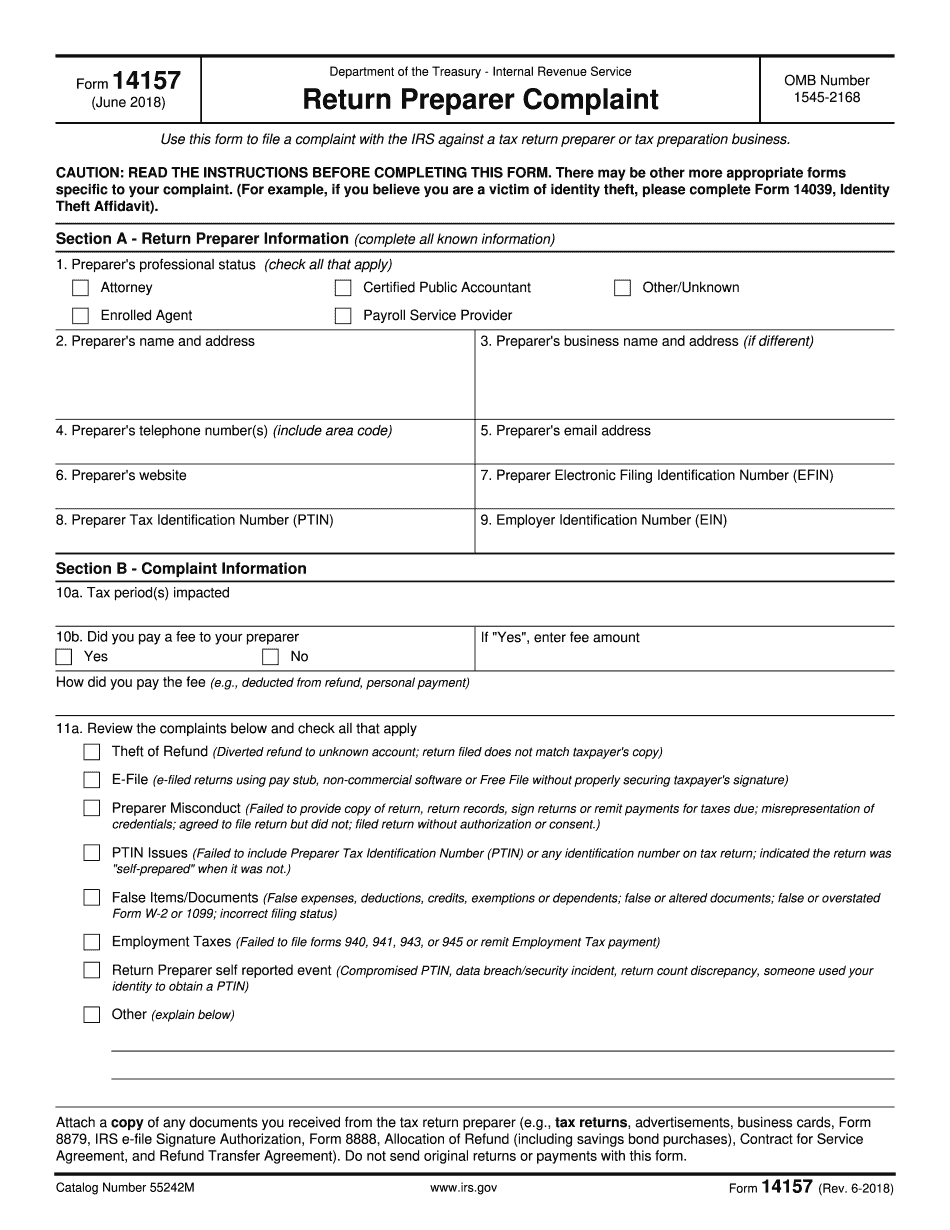

Form 14157 is a Complaint Referral form that is used by the Internal Revenue Service (IRS). The form is used when a taxpayer or a tax professional notices fraudulent or suspicious activity involving taxes, such as identity theft, tax preparer fraud, or falsified documents. This form is necessary for anyone who wants to report fraud or misconduct associated with their tax returns or someone else's. Anyone can fill the form out, including taxpayers, tax professionals, or employees of the IRS. It is essential to fill out the form correctly, as this will ensure that the IRS properly investigates the complaint. Form 14157 is available for download on the IRS website, and it should be submitted by mail or fax to the IRS's fraud department. The form is essential as it enables the IRS to protect tax revenues and take action against any tax fraud and misconduct that it detects.

What Is tax preparer fraud?

Online technologies enable you to organize your file administration and strengthen the productivity of the workflow. Follow the short information in an effort to complete IRS tax preparer fraud, stay away from errors and furnish it in a timely way:

How to fill out a 14157 Irs Form?

-

On the website containing the form, click on Start Now and go for the editor.

-

Use the clues to complete the relevant fields.

-

Include your personal details and contact details.

-

Make certain that you choose to enter proper data and numbers in proper fields.

-

Carefully verify the data in the form so as grammar and spelling.

-

Refer to Help section in case you have any concerns or contact our Support staff.

-

Put an digital signature on your tax preparer fraud printable while using the support of Sign Tool.

-

Once the form is completed, press Done.

-

Distribute the ready blank by way of electronic mail or fax, print it out or save on your device.

PDF editor lets you to make improvements towards your tax preparer fraud Fill Online from any internet linked device, customize it according to your needs, sign it electronically and distribute in several ways.

What people say about us

It's a good idea to send forms on the internet

Video instructions and help with filling out and completing Form 14157